In the modern global economy, the value of a single currency unit has become one of the most discussed topics at kitchen tables and in high-level economic forums alike. To truly understand the state of global inflation and the standard of living, we initiated what we call “The $100 Grocery Challenge.” The premise is simple: What does a fixed budget of $100 USD actually buy in different corners of the world in 2026? By looking beyond abstract Consumer Price Index (CPI) percentages and focusing on the physical volume of a grocery cart, we can uncover the raw reality of purchasing power. This journey across five continents reveals not just the cost of calories, but the shifting definitions of food security and the economic resilience of households worldwide.

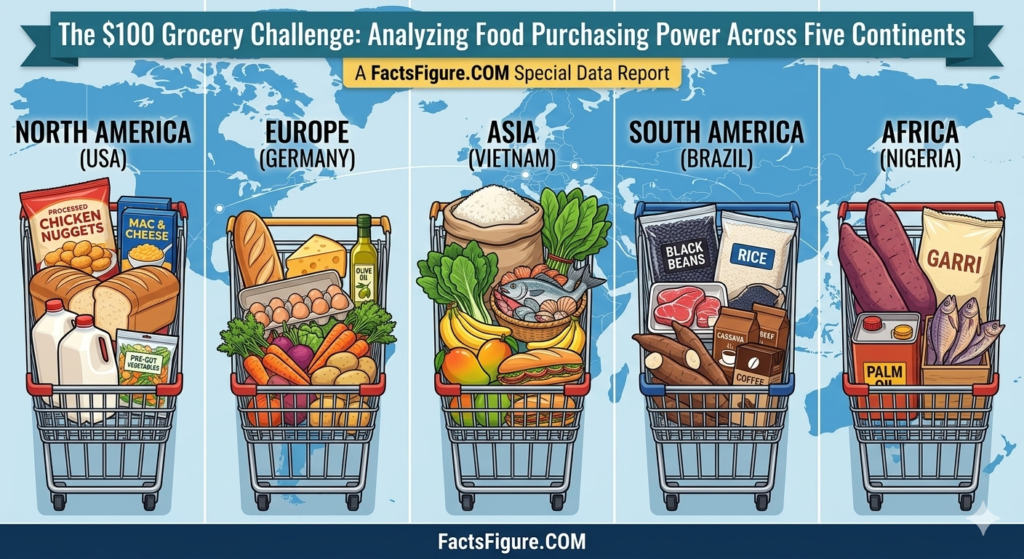

Infographic comparing a weekly grocery cart in 2026 for a $100 USD budget across five continents: North America, Europe, Asia, South America, and Africa.”

North America: The Struggle of the Middle-Aisle Consumer

Starting in the United States, specifically in a mid-sized urban area, the $100 bill feels remarkably lighter than it did five years ago. In 2026, the North American grocery experience is defined by the soaring costs of processed goods and animal proteins. A century-note at a typical supermarket now struggles to cover a full week’s worth of balanced nutrition for a family of four. We observed that the budget is quickly consumed by “pantry staples” like eggs, milk, and bread, which have seen double-digit increases due to supply chain complexities and domestic labor costs.

The strategy for the American consumer has shifted toward “private label” dominance. Shoppers are increasingly abandoning heritage brands in favor of store-owned labels to keep their carts full. While fresh produce remains relatively accessible compared to other regions, the “hidden costs” of convenience—pre-cut vegetables or ready-to-eat meals—have become luxuries that many are now stripping away. The $100 challenge in North America highlights a growing divide: the ability to eat “fresh” is increasingly tied to the ability to spend significant time on meal preparation, as the premium for convenience has reached an all-time high.

Europe: Quality vs. Quantity in a High-Energy Economy

Crossing the Atlantic to Western Europe, the $100 budget (roughly 92 Euros) tells a different story, one heavily influenced by regional agricultural subsidies and high energy costs. In countries like France or Germany, the basket looks significantly more diverse in terms of fresh produce and dairy, but the volume is restricted. European consumers benefit from shorter supply chains for local produce, keeping the cost of seasonal fruits and vegetables somewhat stable. However, the energy crisis of the mid-2020s has left a permanent mark on anything requiring cold-chain logistics or intensive greenhouse farming.

The European “grocery basket” is smaller but often carries higher nutritional density. We found that the $100 challenge here favors the “market-style” shopper—those who avoid large supermarkets in favor of local bakeries and greengrocers. The cost of meat and specialized dairy is substantially higher than in North America, leading to a natural shift toward plant-based proteins. For the European household, the $100 budget is a lesson in precision; there is very little room for waste, and every gram of food is accounted for in the daily caloric budget.

Asia: The Great Divergence of Emerging Markets

In Southeast Asia, using Vietnam as a focal point, the $100 budget undergoes a dramatic transformation. Here, $100 (approximately 2.5 million VND) remains a substantial amount of money for a weekly grocery run, but the “inflationary creep” is beginning to show in imported goods and fuel-dependent deliveries. In a traditional wet market, $100 can still buy an immense volume of fresh vegetables, rice, and local seafood—enough to feed a large multi-generational family for over a week.

However, the divergence happens when the consumer enters a modern, air-conditioned supermarket. The gap between “local market prices” and “supermarket prices” has widened. As the middle class grows, the demand for food safety and branded packaging has driven up costs. For the Vietnamese consumer, the $100 challenge reveals a transitional economy. You can live like a king on local staples, but as soon as you opt for globalized food standards or “Western” imports like apples or cheese, the purchasing power of that $100 evaporates almost as quickly as it does in New York.

Africa and South America: The Volatility of the Commodity Basket

In regions like Brazil or Nigeria, the $100 grocery challenge is a stark reminder of the volatility of global commodities. In Brazil, a major food exporter, the local cost of beef and soy remains a point of domestic tension. The $100 budget here is a battle against the “export-parity” pricing—where local consumers have to compete with international prices for their own homegrown food. The basket is rich in staples like beans and cassava, but the cost of “finished” goods—anything in a box or a can—has skyrocketed due to packaging and transportation costs.

In the African context, the challenge is often one of infrastructure. $100 in a major city like Lagos buys significantly less than it does in rural areas, primarily due to the “last-mile” delivery costs. The budget is heavily weighted toward energy-dense staples like yams and rice. The data shows that in these regions, a staggering percentage of the $100 goes toward the “basics of the basics,” leaving almost nothing for dietary variety or “treat” items. The $100 challenge in these continents is not about lifestyle adjustments; it is a fundamental struggle for caloric stability in the face of currency fluctuations.

The Global Consensus: A Return to Foundational Eating

When we compare the results of the $100 Grocery Challenge across all five continents, a clear global trend emerges: the world is returning to “foundational eating.” Regardless of the country, consumers are stripping away the “excesses” of the 2010s. The commonalities are striking. We see a universal increase in the consumption of legumes and grains, a global reduction in red meat purchases, and a widespread rejection of “ultra-processed” convenience foods that carry high price tags.

The purchasing power of $100 is no longer just a measure of a country’s wealth; it is a measure of its “food resilience.” Countries with strong local agricultural bases and short supply chains are faring much better in the $100 challenge than those reliant on globalized, fuel-heavy logistics. For the reader of factsfigure.com, the takeaway is that our relationship with the grocery store has changed from a place of “infinite choice” to a place of “strategic selection.”

Finding the Personal Path Through the Data

Reflecting on this global data, I’ve realized that the “winners” of the $100 grocery challenge are those who have adapted their lifestyles to the local reality. The most successful households aren’t the ones looking for the cheapest version of a global product; they are the ones leaning into the most abundant local resource. In a world where inflation seems to be a permanent fixture, the ultimate “fact” is that purchasing power is as much about our habits as it is about the numbers in our bank accounts.

By embracing seasonal eating, reducing our reliance on global imports, and rediscovering the efficiency of bulk staples, we can reclaim some of the power that inflation has taken away. The $100 challenge is a sobering look at our current economy, but it also highlights the incredible ingenuity of humans to feed their families, no matter the cost. As we move forward, the “facts” will continue to change, but the “figure” that matters most is our ability to adapt and thrive in an ever-shifting global marketplace.