In an era defined by hyper-consumerism and the relentless pursuit of “more,” the concept of minimalism has emerged not just as a lifestyle aesthetic, but as a sophisticated economic strategy. While many view minimalism through the lens of decluttering or Zen-like simplicity, its true power lies in its ability to fundamentally alter an individual’s balance sheet. By shifting the focus from accumulation to utility, minimalism introduces a “stealth” form of wealth creation. This editorial explores the quantitative side of reduced consumption, analyzing how a minimalist framework can accelerate financial freedom and redefine the very metrics of a successful life in 2024.

The Economics of Minimalism…

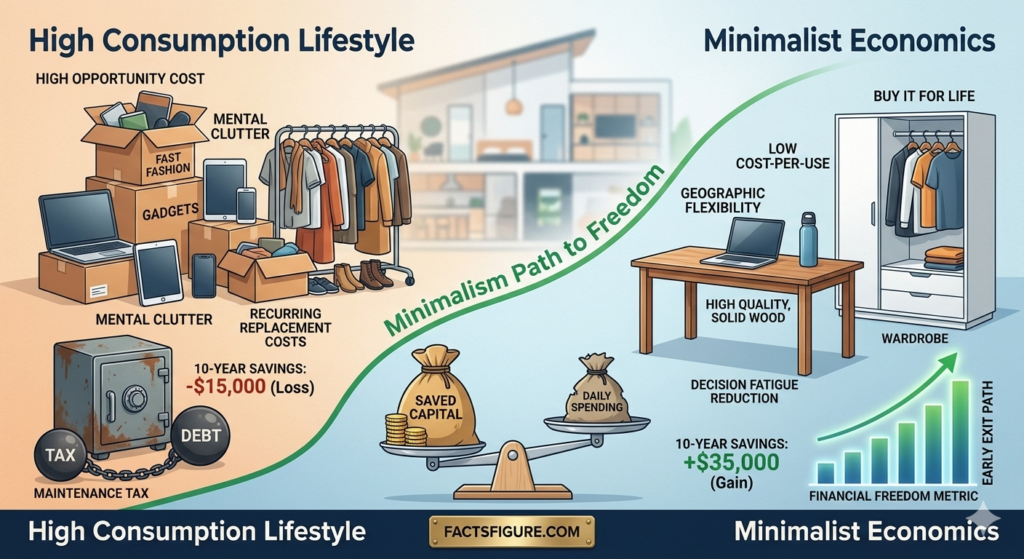

The Opportunity Cost of the Accumulated Object

Every item we own carries a hidden economic weight known as opportunity cost. When we spend capital on a non-essential asset—be it a trendy gadget or a piece of fast fashion—that money is immediately stripped of its potential to generate future wealth. In the world of high-interest savings and compound growth, a $1,000 purchase today isn’t just $1,000; it is the $5,000 or $10,000 it could have become over a decade of investment.

Minimalism forces a confrontation with this reality. By reducing consumption, an individual effectively “reclaims” their future capital. Instead of managing a growing inventory of depreciating assets, the minimalist focuses on liquidity. This shift in mindset transforms the household from a center of consumption into a center of capital preservation. When we calculate the financial freedom gained, we aren’t just looking at the money saved on the price tag; we are calculating the decades of “time” bought back through the power of compounded returns on that unspent capital.

The Hidden Drain: Maintenance, Storage, and Mental Tax

A central fact often overlooked in traditional economics is the “carrying cost” of ownership. Every physical object requires a combination of space, maintenance, and mental energy. A larger wardrobe requires a larger closet, which in turn requires a larger (and more expensive) living space. Electronics require updates, repairs, and eventual recycling. These micro-expenses, when aggregated over a lifetime, form a significant drain on a household’s net worth.

Minimalism operates on the principle of “subtraction for growth.” By owning fewer, higher-quality items, an individual drastically reduces these hidden costs. The financial freedom gained here is structural. It allows for “geographic flexibility”—the ability to live in smaller, more efficient spaces in high-value urban areas without feeling cramped. Moreover, the reduction in “decision fatigue” associated with managing an overabundance of choices leads to greater professional focus. In this sense, the economics of minimalism are as much about maximizing human capital as they are about saving currency.

Breaking the Cycle of Hedonic Adaptation

One of the greatest enemies of financial freedom is hedonic adaptation—the observed tendency of humans to quickly return to a relatively stable level of happiness despite major positive or negative events or life changes. In consumer terms, this is the “high” we feel after a new purchase, which inevitably fades, prompting us to buy something else to regain that feeling. This cycle is an economic treadmill that keeps even high-earners in a state of perpetual financial fragility.

Minimalism provides the psychological tools to break this cycle. By consciously practicing reduced consumption, we recalibrate our “happiness baseline.” We begin to find utility and joy in experiences and relationships rather than in the novelty of new objects. From a financial standpoint, this is the ultimate “hedge” against inflation and market volatility. If your happiness is not tied to the constant acquisition of new goods, you become immune to the social pressures of “keeping up with the Joneses,” a phenomenon that has historically led to unsustainable levels of consumer debt.

The “Buy It For Life” Metric: Quality as a Financial Guardrail

Minimalism does not mean owning nothing; it means owning the right things. The economic shift here is from “quantity” to “durability.” The minimalist often spends more on a single item—a high-quality coat, a solid wood desk, or a professional-grade tool—than a typical consumer. However, the “Cost-Per-Use” (CPU) of these items is significantly lower.

While a “fast-fashion” shirt might cost $20 and last ten washes (a cost of $2 per wear), a $200 high-quality alternative might last five hundred washes (a cost of $0.40 per wear). Over a decade, the minimalist spends less, generates less waste, and enjoys a superior product. This is a form of “defensive investing.” By prioritizing durability, the individual protects their future self from the recurring costs of replacement, effectively locking in a lower cost of living for years to come.

Quantitative Freedom: The Math of the “Early Exit”

The ultimate goal of the economics of minimalism is the “Early Exit”—the point at which passive income or modest savings can support a simplified lifestyle. The math is straightforward but profound. If you can reduce your monthly essential spending by 30% through minimalist practices, you don’t just save 30% of your income; you reduce the “target number” required for financial independence by that same 30%.

This reduction in the “retirement threshold” can shave a decade or more off a traditional working career. Financial freedom, in this context, is not about having millions in the bank; it is about the gap between your needs and your resources. Minimalism widens that gap from both ends—by increasing your savings rate and simultaneously lowering your cost of existence. It is the most accessible path to autonomy in the modern world, requiring no high-frequency trading or complex real estate deals—only the discipline to say “no” to the non-essential.

Conclusion: Wealth as a State of Autonomy

Ultimately, the economics of minimalism redefine wealth as a state of autonomy rather than a collection of trophies. In a world that constantly tries to convince us that our value is tied to our volume of consumption, choosing to own less is a radical act of financial rebellion. It is a calculated move to prioritize the “intangible” over the “tangible”—freedom over furniture, time over trinkets.

For the facts-driven reader of factsfigure.com, the numbers are clear. The financial freedom gained from reduced consumption is not a myth; it is a measurable, reproducible result of disciplined living. By embracing the minimalist framework, we don’t just save money; we buy back our lives. We move away from being cogs in a consumption machine and toward being the architects of our own time. In the final calculation, the things we don’t buy are the very things that set us free.