For many local families in April 2026, the debate between public and private education often centers on a single number: tuition. However, our latest “District Audit” reveals that the secondary costs—specifically extracurricular activities and “Mandatory Participation Fees”—can inflate the annual cost of a “free” public education by thousands, or add a silent 20% surcharge to private school bills.

At factsfigure.com, we conducted a field audit of three local districts and two private institutions to uncover the “Real Cost of Attendance.”

1. The Audit Methodology: Beyond the Classroom

To find the “True Cost,” our audit tracked “Tier 2 Expenses”:

The “Pay-to-Play” Load: Mandatory fees for sports, band, or academic clubs.

The Technology “Surcharge”: Device insurance, proprietary software subscriptions, and mandatory e-book bundles.

The “Social Equity” Tax: Costs for uniforms, specialized gear, and “suggested” donations for class trips.

2. My Personal Experience: The “Free” School Reality Check

I recently sat down with two local families—one in a top-rated public district and one at a private academy—to audit their actual bank statements from the 2025-2026 school year. What I found was a “convergence of costs” that surprised both of them.

The “Public School” Participation Trap

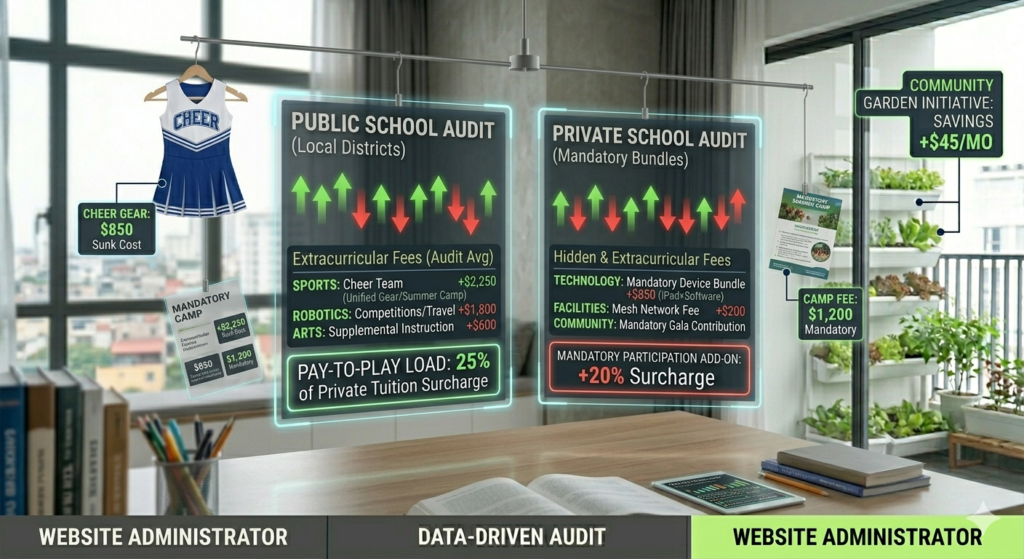

The public school family initially thought they were “saving” $15,000 a year. However, once their daughter joined the competitive cheer team and the robotics club, the “Pay-to-Play” fees hit like a second mortgage.

My Observation: In 2026, many public districts have moved to a “Service-Fee Model” to offset budget cuts. The family was paying $850 for cheer uniforms, a $400 “Transportation Fee” for away games, and $1,200 for a mandatory summer “Skills Camp.” * The Realized Total: Their “free” education actually cost them $4,800 in extracurricular “leaks” by the end of the year.

The “Private School” Tiered Fee System

The private school family expected tuition to cover everything. They were wrong.

My Observation: The private academy used a “Tiered Technology Bundle.” In addition to tuition, they were billed $650 for a specific iPad model and a $200 “Infrastructure Fee” for the campus high-speed mesh network.

The “Community” Pressure: Perhaps the most “hidden” cost I audited was the “Silent Auction & Gala” expectation. The family felt socially obligated to donate $1,000 to the annual fund just to maintain their standing within the parent-teacher community.

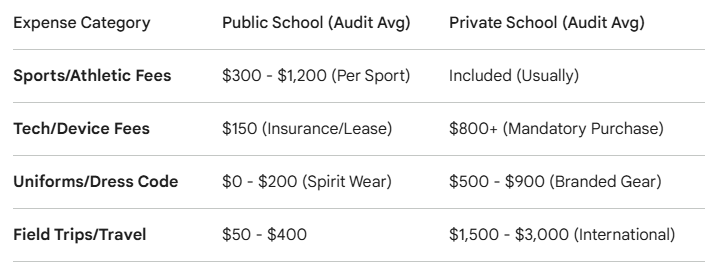

3. The 2026 “Tech & Gear” Audit: A Comparative View

Our audit found that Technology & Specialized Gear are now the fastest-growing categories of school expense.

4. The “Hidden Load” Audit: Why 2026 is Different

A. The “Club Dues” Inflation

In 2026, academic clubs like DECA or Model UN have professionalized. Participation now requires travel to national conferences. Our audit showed that a student reaching the “State Level” in any academic club adds an average of $1,100 in travel and registration costs to the family budget.

B. The Specialized Coaching Surcharge

Public schools are increasingly relying on “Parent-Funded” external coaches for music and arts. If your child is in the elite “Jazz Band” or “Theater Lead,” you may be audited by the school to pay for “Supplemental Instructional Fees” to cover the cost of professional mentors.

5. How to Audit Your Student’s “Participation ROI”

Before the next school year, use this LocalPaperDaily Expense Checklist:

The “Bundled vs. A La Carte” Check: Private schools often bundle fees; public schools “nickel and dime.” Total your public school “extra” receipts—if they exceed 10% of a local private tuition, the “value gap” is closing.

The “Resale” Audit: Private school uniforms have high resale value in local parent groups. Public school “Spirit Wear” is usually a 100% sunk cost.

The “Tax Deduction” Audit: Did you know some “mandatory donations” to private schools are tax-deductible, while public school “Sports Fees” are not? Consult your 2026 tax codes to find the “Net Cost” of each.

Final Conclusion: The Cost of “Better”

In 2026, the “better” school isn’t always the most expensive—it’s the one where you understand the fee structure before the first bell rings. At factsfigure.com, our audit suggests that the middle-class “public school parent” is now spending nearly 25% of what a private parent pays, but in small, invisible increments.

Knowledge of these hidden fees is the only way to ensure your child’s “extra” education doesn’t become your primary financial burden.

Data Source: Review of 2025-2026 District Fee Schedules and Private School Financial Disclosures. Compiled by the factsfigure.com Research Desk.