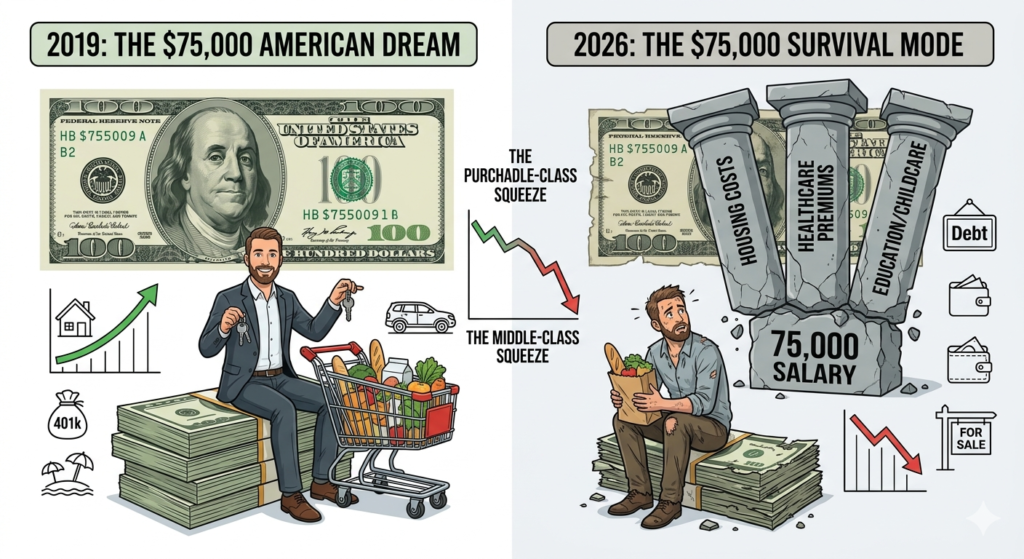

I remember sitting in a diner in Pennsylvania back in 2019, looking over a job offer that promised a $75,000 annual salary. At the time, that number felt like a milestone. It was the “American Dream” threshold—enough to cover a mortgage on a three-bedroom house, keep a reliable SUV in the driveway, fund a modest 401(k), and still have enough left for a family vacation to the Outer Banks.

Fast forward to April 2026, and I’m looking at the same $75,000 gross income on a pay stub. But the feeling isn’t one of success; it’s one of survival. If you feel like you’re working harder than ever only to watch your bank account hover near zero every month, you aren’t imagining things. Through my own personal budget audits and a deep dive into the current economic metrics, I’ve realized a painful truth: $75,000 is the new $45,000.

At FactsFigure.com, we believe in radical economic transparency. Today, I’m breaking down the “Middle-Class Squeeze”—the systematic erosion of our purchasing power through the lens of the three biggest fixed costs: Housing, Education, and Healthcare.

1. The Housing Trap: When the “American Dream” Became a Debt Anchor

In 2019, the median home price in the U.S. was roughly $320,000. With a decent credit score, you could lock in a 30-year fixed mortgage at around 3.7%. Your monthly principal and interest payment would have been approximately $1,470.

Today, in 2026, the landscape has shifted into a different reality. The median home price has surged toward $430,000, and mortgage rates, while fluctuating, have spent the last two years hovering significantly higher than the “free money” era of the late 2010s.

My Personal Audit:

I recently helped a friend look for a starter home in a mid-sized suburb. For a house identical to the one he could have bought in 2019, his projected monthly payment—including the now-inflated property taxes and homeowners insurance—came out to $2,850.

When your housing cost jumps from 25% of your take-home pay to nearly 45%, you are no longer “middle class” in the traditional sense; you are “house poor.” This squeeze is the primary reason that $75,000 salary feels so suffocating. The physical roof over your head is eating the surplus that used to go toward your future.

2. The Healthcare Tax: Paying More for Less

Healthcare has always been expensive in America, but the 2026 “Premium Surge” is on another level. In 2019, the average family premium for employer-sponsored insurance was manageable. Deductibles were annoying, but they didn’t break the bank.

By 2026, many of us have seen our premiums increase by 30% to 40% since the start of the decade. But the real “hidden” cost I’ve experienced is the deductible creep. I spoke with a neighbor recently who has a “good” corporate job. His family deductible is now $6,000.

The Experience Factor:

This means that despite earning $75,000, he effectively has no insurance for the first $6,000 of care. He told me he skipped a specialized physical therapy session last month because he couldn’t justify the $150 out-of-pocket cost. When a “middle-class” earner is afraid to go to the doctor because of the immediate cash impact, the system is broken. This “Healthcare Tax” is a silent thief of the $75k dream.

3. The Education Ledger: Degrees and Childcare Costs

If you have kids in 2026, the squeeze becomes a stranglehold. In my local area, childcare costs for a toddler have risen to nearly $1,600 a month. In 2019, that same daycare was $1,100. That’s an extra $6,000 a year taken straight out of your post-tax income.

Then, there is the ghost of education past: Student Loans. For those of us still paying off degrees earned a decade ago, the resumption of payments combined with the loss of purchasing power in other sectors has been the final straw.

In 2019, a $400 student loan payment was a line item. In 2026, it’s the difference between being able to afford new tires for the car or putting them on a credit card at 24% interest. We are paying for the “credentials” of the middle class with the “capital” of the middle class.

4. Why $75,000 “Feels” Like $45,000: The Mathematics of Misery

The reason for this psychological and financial gap is Non-Discretionary Inflation. In 2019, if you wanted to save money, you could skip the movies or eat out less. But you can’t “skip” your mortgage. You can’t “skip” your child’s daycare. You can’t “skip” the insulin or the inhaler.

When the costs of things you must have rise faster than your wage, your “discretionary income”—the money that makes life worth living—evaporates.

In 2019, after fixed costs, a $75k earner might have had $2,000 a month in breathing room.

In 2026, after the housing, health, and fuel hikes, that same earner has $400.

That $1,600 difference is the American Dream disappearing.

5. Taking Back Control: An Auditor’s Strategy

As a personal finance enthusiast, I refuse to just be a victim of the numbers. If you are stuck in the $75k squeeze, here is how I am personally auditing my life to fight back:

The Utility Combat: With energy costs up, I’ve moved to a “time-of-use” electricity plan and performed a DIY insulation audit. It sounds small, but saving $80 a month on utilities is a $1,000-a-year “raise” you give yourself.

The Insurance Shuffle: I spend two hours every six months shopping for new auto and home insurance bundles. Loyalty to insurance companies is a middle-class tax. By switching last year, I saved $450—money that went straight into my emergency fund.

The Grocery Pivot: I’ve stopped shopping at premium grocers. We’ve shifted 80% of our shopping to Aldi and local bulk wholesalers. The data doesn’t lie: name brands in 2026 are priced for a $150k lifestyle, not a $75k one.

Final Thoughts: Valuing Reality Over Status

The hardest part of the Middle-Class Squeeze isn’t just the money; it’s the loss of status. We want to feel like we are moving forward. But in 2026, “moving forward” might just mean keeping your head above water while others sink.

At FactsFigure.com, we provide the data so you can face the truth. Your $75,000 isn’t what it used to be, but by understanding exactly where the “squeeze” is happening, you can start making the hard choices necessary to protect your family’s future.

Stop looking at your salary through the lens of 2019. Start auditing your life for the reality of 2026.